Editor’s note: The markets and our Chaikin Analytics offices will be closed Monday, February 20, for Presidents Day. So we won’t publish our Chaikin PowerFeed e-letter that day. Look for your next issue on Tuesday, February 21.

The “sharks” are circling Salesforce (CRM)…

Salesforce is known for its mega-suite of customer-relations management (“CRM”) software. It lets customers do all sorts of things on their own…

CRM software users can manage sales leads, customer accounts, approvals, marketing campaigns, and much more. And they can do it all with just a few clicks of the mouse.

Salesforce also helped introduce the world to the idea of Software as a Service (“SaaS”). Without SaaS, we would all still need monstrous programs installed on our computers.

But lately, Salesforce has been struggling…

From 2013 to 2022, the company’s annual sales averaged about 30% growth. But that growth slowed to 20% in the trailing 12 months. And it was only 10% in the latest quarter.

Salesforce’s operating margins and return on equity are getting weaker, too.

The company is now laying off workers and buying back shares to cut costs. And as we’ll discuss today, it’s also getting attention from a few “sharks” – or activist investors…

In short, activist investor Starboard Value announced a stake in Salesforce on October 18. And then, Elliott Management revealed its presence on January 23.

These activists are still fleshing out their plans. But to me, their interest is for one reason…

It’s about Platform as a Service (“PaaS”).

SaaS involves finished software products that customers can use. Salesforce made a name for itself with its CRM software, which is a SaaS offering.

PaaS is very different. It’s about helping folks build things even if they don’t know programming languages. Instead, they can use simpler, “low code” objects.

In other words, given their acronyms, PaaS and SaaS might sound similar. But in reality, they serve different types of customers who want to do different things.

Here at Chaikin Analytics, we use PaaS behind the scenes with the Power Gauge.

Folks who use our SaaS-like platform see Power Gauge content that looks like this…

It’s easy to understand. It’s visually appealing. And it’s a finished product that you can use.

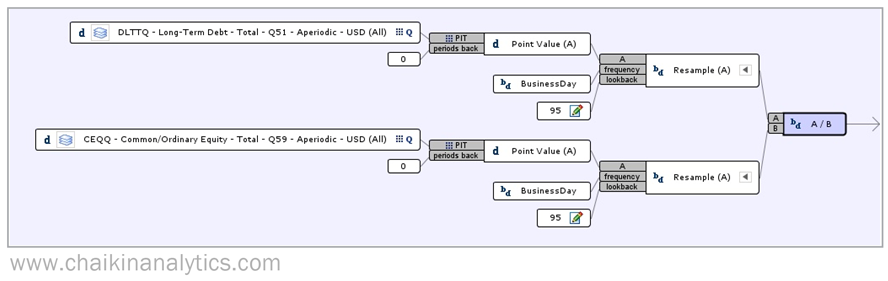

But behind the scenes, we make it all work with PaaS. For example, here’s the low-code way to display one of our simplest items – the ratio of long-term debt to equity…

But that data alone doesn’t make it a Power Gauge factor…

From there, we need to attach another “concept” to calculate its rank. Then, we combine it with 19 other ranked factors to create the Power Gauge’s overall grade. And finally, we use more complex steps to compute everything and send it over to our user-friendly platform.

In recent years, Salesforce has spent a lot of money on PaaS-focused efforts…

The company paid $6.5 billion to acquire MuleSoft in May 2018. A little more than a year later, it paid $15.7 billion for Tableau. And in July 2021, it bought Slack for $27.7 billion.

That’s nearly $50 billion overall. It’s a worthwhile cause… but it’s costly.

Now, I can’t say if the activist investors will make Salesforce spin off its PaaS. (I hope they do. I love PaaS and might invest in it as a separate company.) But at a minimum, I believe they will at least do something to improve management’s investment and cost discipline.

And Wall Street seems to agree…

Salesforce’s stock is up about 8% since Elliott, the second activist, got involved.

The Power Gauge helps us see that the “smart money” is behind the company as well. Remember, our Chaikin Money Flow indicator tracks that. And it’s firmly in the green zone.

Even better, you can see in the screenshot above that the Power Gauge is “bullish” overall.

The sharks are circling Salesforce. And they’re pushing for much-needed changes.

That bodes well for the company’s long-term turnaround. Consider adding shares today.

Good investing,

Marc Gerstein