Suddenly, utilities are darlings of the market…

It all started with a “growth in demand” story. Everything is increasingly going electric – especially cars. That means a step up in electricity demand.

Then the AI and cryptocurrency bandwagon rolled into town. These technologies need huge data centers that suck up massive amounts of power. That means even more growth.

And just when it started to look like things couldn’t get any better, the so-called “Magnificent Seven” mega caps whiffed. Stocks got volatile. And utilities were a safe harbor in the storm.

They were cheap, defensive, and they paid dividends. In short, they were everything the Magnificent Seven weren’t.

But in finance, growth and safety seldom go hand in hand…

If an investment is safe, it usually doesn’t grow that much. And if an investment is growing, it usually carries more risk.

So where does that leave us with utilities?

Put simply, you can believe in the safety with utilities… but not in the off-the-charts growth.

Utilities operate under agreements called regulatory compacts. These agreements grant utility companies monopoly status in a particular state or region.

With a regulatory compact, a utility gets a guaranteed return of capital. It also gets a (mostly) guaranteed return on that capital.

In exchange for this, the regulator gets a say in how much capital gets invested. And it gets a say in how that money gets spent.

So according to the “growth in demand” story, the increase in demand means a lot more capital. And that would mean a lot more return on that capital.

But the problem is that the demand isn’t skyrocketing yet. Demand from electric vehicles (“EVs”) and data centers is still just a drop in the bucket.

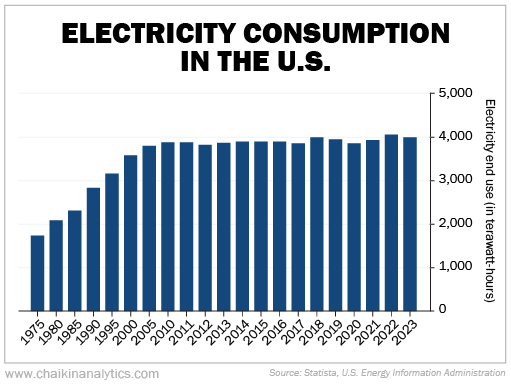

In the chart below, you can see that America’s electricity end use hasn’t grown in the past decade…

The American Public Power Association tracks U.S. electricity demand. It pegs the incremental demand from EVs and data centers at about 300 terawatt-hours… by 2030.

That’s a 7.5% increase on the roughly 4,000 terawatt-hours currently used per year. So that increase would be spread over seven years.

To be sure, that’s growth… but not a massive amount. So let’s look at safety…

Regulatory compacts make it hard for utilities to go bankrupt. No state wants to leave its citizens in the dark.

In response to its liability for wildfires in California, PG&E (PCG) did declare bankruptcy in 2019. But the state stepped in quickly. And the lights stayed on.

If there’s anything to worry about, though, it’s leverage. Utility companies carry a lot of debt.

The average debt-to-equity ratio for companies in the S&P Utilities Select Sector Index is 1.7. Debt to total capital for these companies is 55%.

But most incremental spending these days is on “network reliability.” That’s in response to natural disasters like hurricanes and wildfires.

Utilities fund that spending through debt known as recovery bonds. And with the blessing of state regulators, the cost of these bonds flows directly to the ratepayers.

Recovery bonds do add to a utility company’s debt. But the ratepayers get the bill.

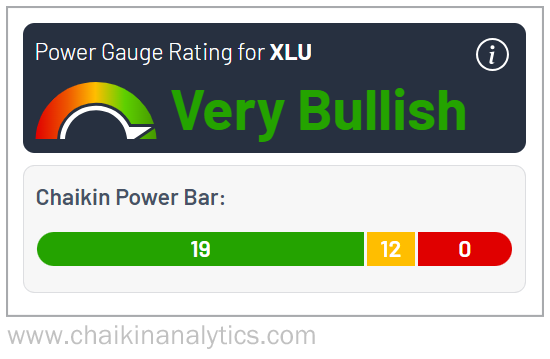

So when it comes to utility stocks, we can track them in the Power Gauge through the Utilities Select Sector SPDR Fund (XLU). As its name implies, it tracks the Utilities Select Sector Index.

So far in 2024, XLU is up roughly 22%. Over the same time frame, the S&P 500 Index is up about 16%. Utilities are outperforming the broad market.

Meanwhile, the Power Gauge gives XLU a “very bullish” rating right now. And as you can see in the screenshot below, the fund has more holdings rated “bullish” or better than “neutral” and “bearish” or worse ones…

So if you’re an investor who favors safety over growth, there’s plenty to choose from.

In general, utilities aren’t an investment that will get you rich. But they can be an investment that might keep you rich.

And for some folks, that’s just fine.

Good investing,

Joe Austin